“Back to the future” with Checkbook.io Blockchain enabled Digital Checks: The end of paper payments.

What is a Blockchain-enabled digital check?

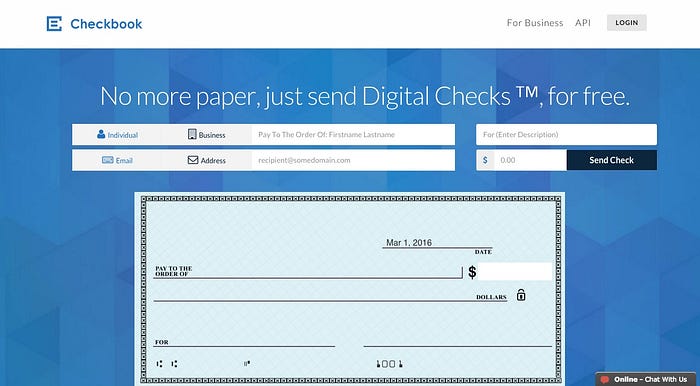

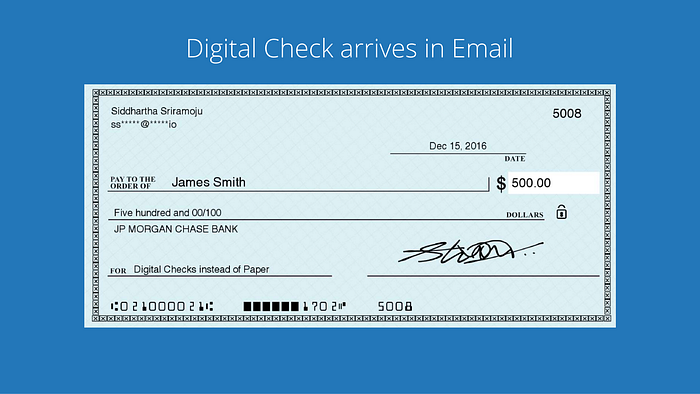

A Blockchain-enabled digital check solution can securely transfer payments online via email. This form of a check is instantly deposited, or you may print and deposit the physical check at a local bank.

A digital check is similar to an electronic check, but they are not the same. In fact, an e-check merely converts check information into an ACH file, and they suffer many drawbacks:

· It is a hassle to fetch routing and account numbers every time you send/receive money

· E-check accounts don’t always update in real-time.

· Funds are not assured three-business-day settlements

In contrast, customers of Digital Checks can confirm their account records in real-time by logging into their financial institutions’ website. So, this means there is no reason to go looking to find your routing or account numbers. Also, Digital Checks can offer overnight settlement using the “Check21” procedure.

What is a Distributed Ledger Technology (DLT)? — The Blockchain

Distributed Ledger Technology, also known as Blockchain Tech is a virtual technology used to record transactions of digital assets where transactions. The records are stored in multiple locations at the same time.

Unlike conventional databases, distributed ledgers do not store central records or administration functionality. In a distributed ledger, every node verifies each item, this produces a record of every detail and creating a consensus on every item’s veracity.

A distributed ledger holds static records, such as a registry of active transactions. This computer architecture has become a widespread revolution in record-keeping on how files are collected and communicated. There are many other advantages of using The Blockchain. The most significant advantage of using Blockchain technology is its resiliency.

Bitcoin has been running for ten years now, without suffering a nanosecond of downtime. That is impressive! Few large-scale enterprise systems can claim to have the same reliability of uptime as The Bitcoin Blockchain. If you are a central bank, I am sure by now you’ve considered moving away from physical cash, and to an electronic money-based software, with zero downtime.

It could also be a way to create greater security and efficiency for online Paper Check payments. The Blockchain also offers improved credibility because of the rules that it enforces.

Problems with using Paper Checks.

Carrying a Paper Checkbook means more bulk and a higher chance of human error. If you somehow misplace your checks, then your account could be in danger.

Your bank account and routing numbers can end up in the wrong hands. When this happens, you better let your bank know right away, and you may also want to keep a close eye on your monthly bank statement, for any unusual or fraudulent activity.

Writing checks is an inefficient hassle.

Just to prepare the Paper Check you need to find it, tear it out of the book, write everything on it neatly, spell out all the numbers, and remember to sign. Plus, if you write a lot of checks, you will need to keep reordering new ones. If you bring your Paper Checkbook anywhere, you are increasing the possibilities of an inconvenience. The cashier may ask you to show identification and other information for verification. With any luck, no one waiting behind you is in a rush!

Balancing checking accounts is a chore.

Some people have the mind to balance their Paper Checkbook right away each time they write a new check, or they pay someone to manage their funds for them. But, most of us that cannot afford a personal accountant is too busy to practice such self-discipline.

Most of us may think of standard mail as a dependable service.

Nevertheless, a shipped Paper Check always seems to move through the system at an extra slow pace. Sometimes, they even get lost or ruined. Paper Checks are sometimes misplaced or stolen in transit, at a store, or at your local bank. The more Paper Checks you write, the more the chances of a problem.

Paper Checks are not cost effective.

As reported by Bank of America, one Business Check costs a company $4 to $20 between the cost of the paper, shipping charges and other administrative tasks associated with processing a Paper Check.

According to Mineraltree Inc., Paper Check costs companies in the USA were somewhere around $25 — $50Bn in 2010 alone. So, why do companies continue to write Paper Checks despite new efficient options that can help companies to save some serious money?

Why most Businesses still write checks.

While familiarity with old ways and reluctance to learn a new technique are two common excuses of — why businesses still write Paper Checks, there are other reasons to consider. For example, a few companies keep on writing checks to leave a trackable paper trail simple and affordable technology-enabled Digital Check solution will help solve this issue.

Customers use products to make their life and job more manageable.

A program that works with no need to read a complicated instruction manual or go through vigorous signup and validation; this will help the less tech-savvy customer become comfortable with modern technology. Then they can begin to see how much money they save by throwing away old checkbooks and switching to Digital Checks.

Few companies lean toward Paper Checks over digital payments because of the remittance advice on Paper Check transactions.

Remittance advice is a slip that comes with a mailed check, it has insight into the payment status of the corresponding check transaction. The problem with the electronic installment remittance advice, there is no standard format; they generate from the payer’s Enterprise Resource Planning (ERP) framework, which is difficult for some small business owners to understand.

Many successful business owners struggle to understand modern technologies.

Naturally, steep learning curves of most technologies is a significant problem. Since there has been no fully automated solution developed for Digital Check payments, the complex nature of digital payments often needs manual intervention. Thus, requiring companies to deal with Digital Check payments on a per transaction basis. At the point when this happens, the versatility which writing a check offers, turns into a convenient incentive, leading customers on to believe they keep more control over their money streams.

To cross this barrier, there should exist a robust framework to process both full and partial installments with start-to-finish electronic payments and does not pause or interrupt the flow, at any point, needing manual human interaction to move those payments on the next step of the bank transfer.

The number one reason people still use Paper Checks.

Finally, the real reason that most people haven’t started taking advantage of the benefits offered by electronic forms of checking has to do with all the headache involved with onboarding new users on the ACH rails. Multiple technical barriers make the process difficult, compromising the user experience for new customers who finally decide to try to receive a virtual bank payment.

First, Consumers are asked to enter their personal bank account, and public routing numbers, which most people do not memorize, or they are skeptical. Many private check users think, by giving the account number, that they are offering full access to their available funds, leaving them vulnerable for unauthorized withdrawals. Even though in some cases this sometimes happens, these numbers are still considered public information and are not made to be kept secret.

Then, to withdraw funds, the consumers still have to verify ownership of their account by reporting the exact amounts the most recent micro-deposits placed into their checking account by the merchant service provider, is found in your recent transactions by logging in to the banks’ website.

Now, if you kept an open mind and stayed patient, you may have made it this far into the ACH onboarding process. Unfortunately, the problems do not stop here. This is the part that turns most people away from digital payments for certain and leaves a lasting negative impression on Digital Check services of all kinds…

You’ve completed the initial verification, and likely even waited a few days after sending all the necessary documents for account ownership to be verified. So, you call to check on the status of your account and the representative places you on what seems to be a never-ending hold. Then, to make matters worse, he comes back on the line and informs you for the first time that it will still take another 3–5 business days for the ACH payment to settle by the bank and be placed into your accounts available funds. This can be catastrophic news for someone who isn’t prepared or was counting on funds being available sooner!

But, aside from the severe negative impact of your payment being postponed due to slow manual processing by the bank, poor practices such as the ones spoke about in this section, can affect the well-being of potentially thousands of potential users or more. But you have to admit to the irony of financial institutions being closed on holidays, when those are the days most notorious for sending annual holiday gifts between family members, in the form of a sentimental card and a Paper Check.

The many strong points of distrust in the banking world must have more to do with people’s unfortunate experiences in the past when dealing with centralized banks. When more companies begin to adopt transparent business models, it may ease these worries and console the trust-issues of those business owners who are still stuck in the Paper Check mindset.

Checkbook.io is the solution to Paper Checks.

The Paper Check system uses a very outdated process. It has been around a long time, and in 2015 the United States alone printed more than 15 billion Paper Checks. Now that is a lot of paper, don’t you agree? This market is vast, but Checkbook.io aim is even further!

Checkbook.io has even started development on a Blockchain solution for sending/receiving Digital Checks more securely. They are working to use the latest technology to combine transparency, security, and reliability to Digital Checks and fix a huge problem for consumers, businesses, and financial services — the outdated Paper Check system.

Their web service makes Digital Checking simple by enabling you to send straight to the recipients’ email, and it requires no software download. Best of all, they do not make you fill out your entire life story to register, in fact, you do not register to use accept deposit transfers instantly into your bank account. The recipient only verifies their bank account, click… click… then funds get credited to that bank account automatically.

So, you do not need to waste any time waiting in a bank line to deposit a manual Paper Check anymore, and do not worry, you be asked to deal with the frustrations of scanning a barcode on your mobile phone — with that same phone, doesn’t that sound crazy? Nope, you need not take a perfect picture of a Paper Check either. All you need is to enter two inputs of a bank accounts information and confirm, it is just that easy!

Checkbook.io works excellent when sending personal, business, and any other check payment, even “direct deposit only” such as American Express Bluebird accounts. The high scaling solution has already helped with class action lawsuits and B2B settlement solutions where hundreds of thousands of checks needed to be sent out.

Since their founding, the Blockchain Enabled Digital Check service has helped over 1 million delighted customers by processing over 2 million Digital Check transactions. If you still have questions, visit the website at www.checkbook.io and start a live chat with 24/7 customer support, or try sending a Digital Check today. It is free!